Regulatory News

Financial results for the year ended 31 December 2019

Brussels, 18 March 2020

The enclosed information constitutes inside information and is to be considered regulated information as defined in the Belgian Royal Decree of 14 November 2007 regarding the duties of issuers of financial instruments which have been admitted for trading on a regulated market.

Cenergy Holdings S.A. (Euronext Brussels, Athens Stock Exchange: CENER), hereafter “Cenergy Holdings” or “the Group”, today announces its financial results for the year ended 31 December 2019.

Record year for profitability, stable backlog going forward

Highlights

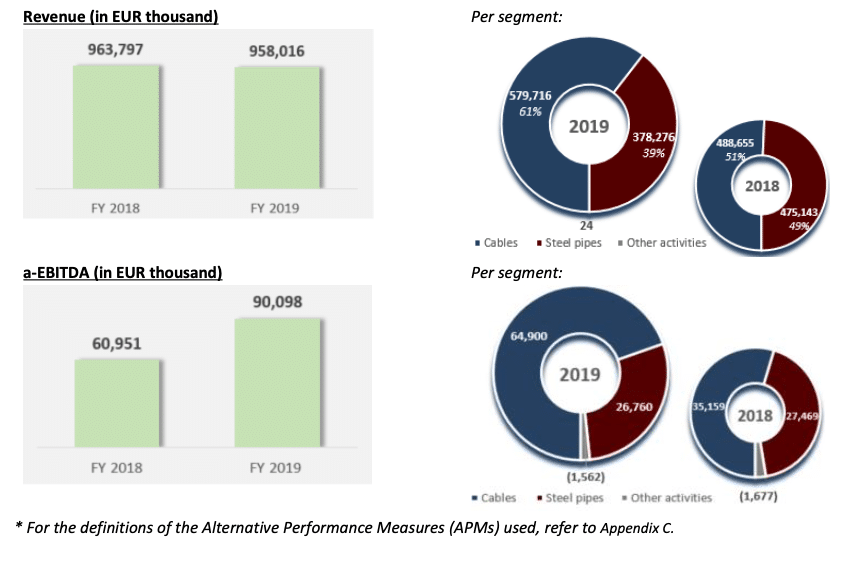

- Very high operational profitability: adjusted EBITDA for 2019 reached EUR 90 million (48% growth year- on-year)

- Cash flow from operating activities for 2019 reached EUR 110 million

- Net debt down by EUR 60 million

- Substantial order backlog of EUR 530 million as of 31 December 2019

- Consolidated profit before tax of EUR 28.5 million vs. a EUR 0.7 in 2018

- Consolidated net profit after tax reached EUR 20.2 million

Overview

2019 was a milestone year for Cenergy Holdings as all key objectives set for that year were realised.

Operational profitability in terms of a-EBITDA reached EUR 90 million versus EUR 61 million in 2018 driven mainly by the successful execution of projects in both segments. This notable increase in profitability allowed the Group to produce significant cash flow from operations (EUR 110 million) and decrease overall net debt by EUR 60 million at the end of 2019, despite continuing, though at a slower pace, the capital expenditure necessary to expand and enhance its production capability and provide its customers with high-end solutions. In fact, the Group invested EUR 53 million in all its production sites during 2019 to further support the key objective of its companies to create value and establish their position as key players in the global energy distribution markets.

Net profit after tax for the Group reached in 2019 EUR 20 million. Although, part of the success could be anticipated given the high order backlog of December 2018 both for the cables and the steel pipes segments, it required important commercial effort in a rather tricky global environment. Thus, segments ensured an equally strong backlog of EUR 530 million for the following years and confirmed the effective execution of the segments’ strategy, namely focusing and delivering high margin, high technology, challenging projects in the energy markets.

In 2019, the cables segment demonstrated, for the first time after the completion of its investment programme in the offshore business that started back in 2011, a solid financial performance and a high utilisation of all its available production lines. Several projects awarded to Hellenic Cables and its specialised submarine cables plant in Corinth, during the last semester of 2018, served as the backbone of a strong 2019 performance, founded on their ability to provide cost-effective, reliable and innovative solutions to changing market needs. Over the year, cable companies executed successfully technically demanding projects in high and extra high voltage, for both subsea and land cables. On the other hand, the cable products business also delivered satisfactory profits, with demand in traditional markets being rather stable, despite challenges faced. The segment’s robust performance was further encouraged by recent initiatives to enter new geographical markets, such as the USA, as well as the persistent determination to be on the forefront of technology with industrial research on developments, such as direct current (DC) cables and dynamic cables for floating offshore wind platforms.

For Corinth Pipeworks, 2019 was a very challenging year: strong protectionism, particularly in the USA, limited considerably the company’s operating field. The company responded to this new environment by focusing on quality and customer satisfaction and managed to maintain market share, while entering new markets and product segments, such as the technically demanding deep offshore market. The subsidiary kept a high utilisation rate for its Thisvi plant and was present in all regional markets, mainly North and South Europe and Eastern Mediterranean.

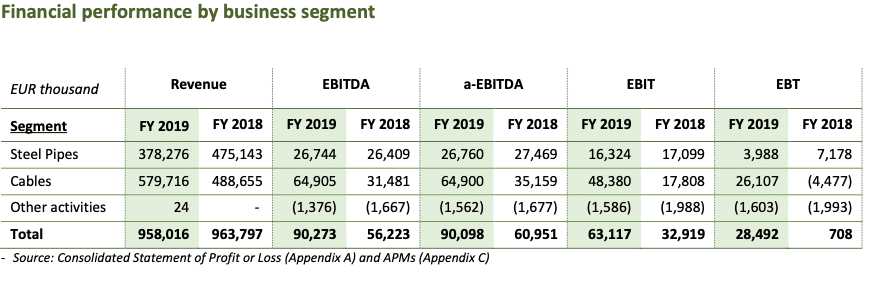

Consolidated revenue for 2019 stands at EUR 958 million, stable compared to 2018. On the contrary, adjusted EBITDA increased by 48% y-o-y to EUR 90 million, with the cables segment realizing a considerable increase of EUR 30 million (EUR 65 million in 2019 vs. EUR 35 million in 2018). The steel pipes segment’s operating profitability was stable at EUR 27 million, without the record sales of the previous year. Corinth Pipeworks opted for a more profitable projects mix, as opposed to keeping a high turnover.

Group net finance costs were higher at EUR 34.6 million (EUR 2.4 million more than 2018) due to higher working capital for steel pipes and some foreign exchange losses in 2019. Following, however, the prior year’s debt reprofiling of EUR 118.7 million, improved interest rates and lower net debt at the end of 2019, the overall financing position of the Group is getting stronger.

A stronger EBITDA and contained financing costs led to a healthy EUR 28.5 million profit before income tax, compared to an almost breakeven 2018 (EUR 0.7 million). This is the third consecutive semester that the Group discloses positive profits before tax (H2 2019: EUR 20.5 million, H1 2019: 8.0 million and H2 2018: 3.2 million).

Profit after tax for the period almost tripled to EUR 20.2 million, compared to EUR 6.9 million in 2018.

To keep core businesses operating at a promising efficiency pace for the future, Cenergy Holdings’ companies continued to invest in them: total capital expenditure for the cables segment reached EUR 42.5 million, while for the steel pipes segment, it equalled EUR 10.9 million.

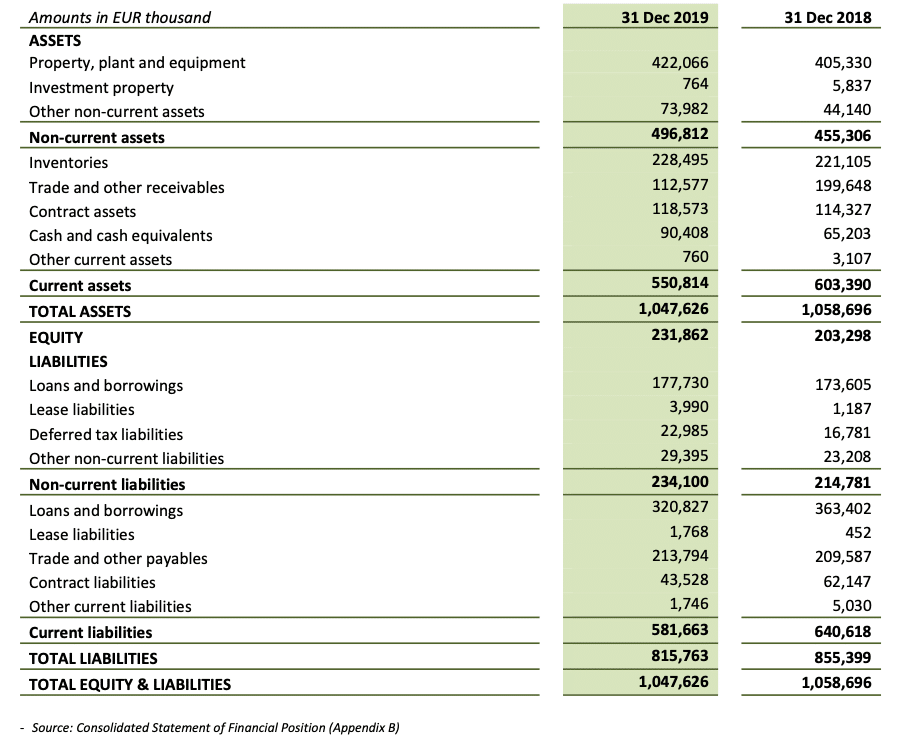

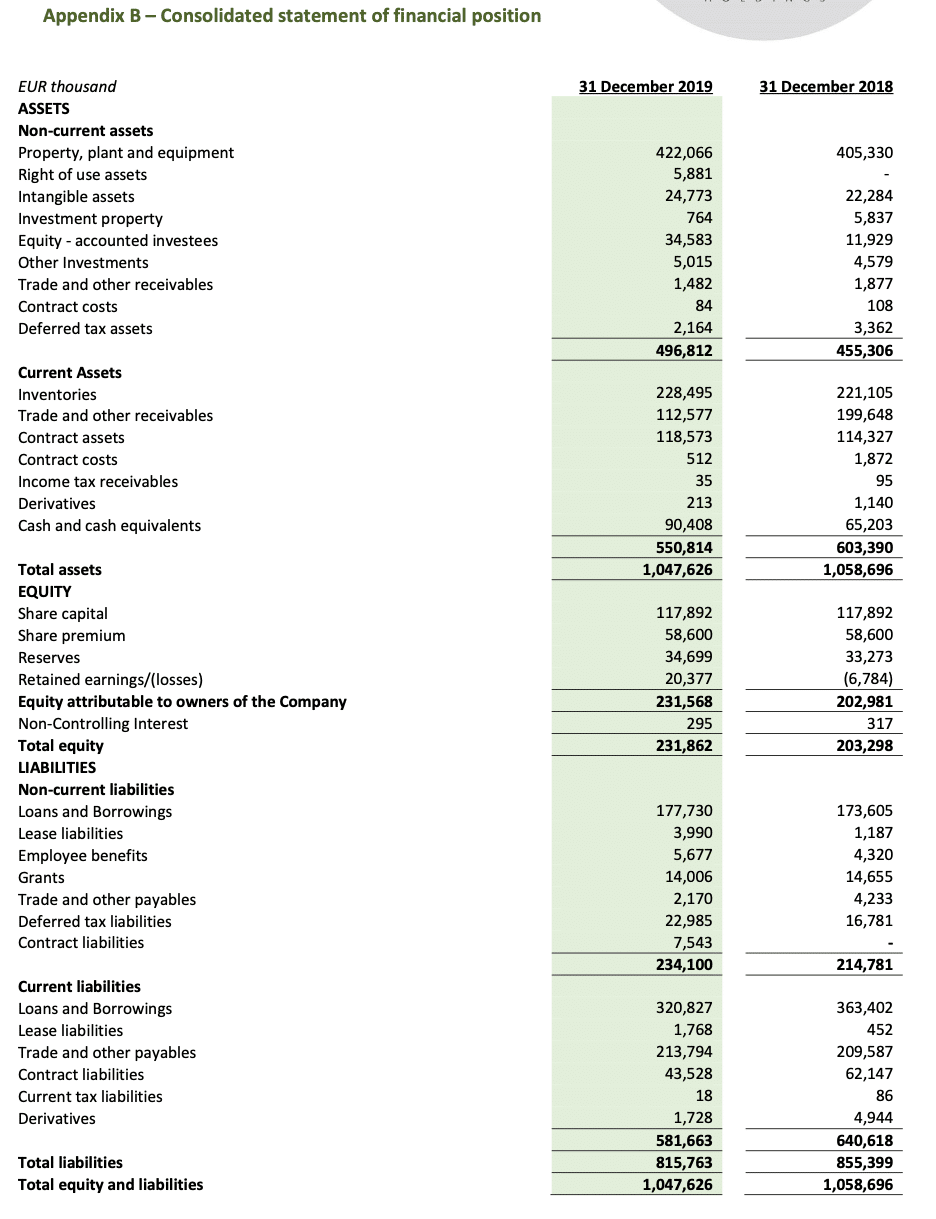

Lower revenue led to lower working capital (incl. contract assets & liabilities): this stood at EUR 195 million on December 31st, 2019, down by 26% y-o-y (EUR 263 million on 31.12.2018). The decrease was driven mainly by collecting a sizeable part of trade receivables outstanding on 31.12.2018, while inventories and trade payables remained at the levels of 2018.

Net debt fell considerably to EUR 414 million on December 31st, 2019 (31.12.2018: EUR 473 million), demonstrating the Group’s commitment to deleveraging. Cenergy Holdings’ debt on that date comprised of long term and short-term facilities, at 36% and 64%, respectively, an improvement versus last year’s mix. All new credit facilities signed during 2019 included much improved credit terms. The effect of IFRS 16 adoption on net debt on December 31st, 2019 was EUR 3.5 million.

Cables

2019 results confirmed a positive performance by all business units in the cables segment, with revenue growth reaching 19%. This growth was particularly supported by the solid performance of the energy projects unit and translated into a profit boost for the whole segment. On the other hand, a high capacity utilisation level for all production units greatly assisted the financial performance of the year, which reached an impressive 85% increase of its operational profitability (adjusted EBITDA) compared to 2018.

2019 for the projects business unit is best portrayed by the following events:

- The extension of the 400kV power grid system in the Peloponnese is on time: production of the extra- high voltage submarine cables was completed in the early summer and, during August 2019, the installation of the first 400kV submarine cable in Greece was completed (seabed clearance, trenching, cable laying and protection) in the Rio-Antirio area.

- The production stages for the Hollandze Kust Alpha project in the Netherlands and for the interconnection of Crete – Peloponnese in Greece started, while those for the second phase of Cyclades islands’ interconnection project in Greece and for the Seamade-Mermaid project in Belgium were concluded. The installation of both projects is expected to take place during 2020.

- The submarine cables for the Modular Offshore Grid project in the North Sea, Belgium and the interconnection of the Kafireas wind park in Evia, Greece, with the national power grid via submarine cables, were successfully finished.During the second half of 2019, Hellenic Cables participated in several tenders across geographical areas and markets and succeeded to secure, among other awards, their first USA project (Mayflower Wind project) with Shell / EDPR and their first contract for inter-array cables with Ørsted, the global leader in offshore wind.The cable products business units achieved steady sales volumes compared to 2018 along but with an improved sales mix. The solid demand from the Balkans, the Middle East and the Nordic countries counterbalanced a slight lag observed in the markets of Germany and Central Europe.Driven by the above, namely, a remarkable progress in the project-based business along with the steady growth in the product-based one, the cables segment exhibited a EUR 30 million increase in adjusted EBITDA, reaching EUR 65 million in 2019, up from EUR 35 million in 2018.

Net finance costs were stable compared to 2018, at EUR 22.2 million. If one excludes foreign exchange effects, they are actually slightly lower (-2%) for the year, as a result of improved interest rates.

Profit before income tax in 2019 was a healthy EUR 26.1 million, compared to a loss of EUR 4.5 million recorded in 2018. Finally, net profit after tax followed the same trend and reached EUR 18.5 million versus losses after tax of EUR 1.3 million in 2018.

The investments in the cables segment amounted to EUR 42.5 million in 2019, largely attributable to:

- the expansion and upgrade of the high voltage submarine cables unit to meet future demand levels;works started during 2018 and were concluded by the end of 2019.

- the initiation of a new investment plan, also in submarine cables, aiming at expanding the inter-array cables production capacity in order to supply offshore wind developers worldwide with a wide range of cables and, more generally, support the growing offshore wind market.The above capital expenditure was financed through the segment’s inflows from operating activities. Free cash flow generated throughout the year was also used to push down the segment’s net debt by more than 12% y-o- y from EUR 291 million on 31.12.2018 to EUR 256 million on 31.12.2019. The determination to restructure long- term debt, securing lower financing costs for the future, continued with measures including, among others, the issuance of EUR 21.4 million bond loans for the submarine cables plant.During 2019, Hellenic Cables has sold its 100% subsidiary Cablel Wires, which had absorbed its enamelled wires sector during the year.Finally, Hellenic Cables consolidated its presence in the USA offshore wind market with the establishment of Hellenic Cables America Inc., a wholly owned subsidiary, providing USA customers with direct support and expertise throughout the entire lifetime of their project.Steel pipesDuring 2019, Corinth Pipeworks produced pipes for Karish, its first deep sea offshore project and an important breakthrough for the steel pipes segment. This was a strategic project in the SE Mediterranean, at a maximum depth of 1,750m, a highly complex work only a few companies worldwide could have accomplished.

In 2019, Corinth Pipeworks was also awarded other major projects, such as:

- Energinet, Baltic Pipe, a 114 km gas pipeline of 32-36” pipes;

- Midia Gas Development Project, a 145 km of 8” & 16” offshore pipeline in Romania;

- Snam, 150 km of gas pipeline of 26” pipes in Italy;

- G.I.G.B. (Gas Interconnector Greece-Bulgaria) project, a 187km gas pipeline of 32” pipes in Bulgaria andGreece.Nevertheless, a difficult USA market, with tariffs on large diameter welded steel pipes exceeding 30% did not allow the segment to reach 2018’s turnover levels. Revenue fell by about 20%, to EUR 378 million, whereas gross profit increased to EUR 31.8 million in 2019, compared to 2018 (EUR 30.8 million) as gross margin, attained in other markets, improved (8.4% in 2019 vs. 6.5%). Adjusted EBITDA remained at the same level, at EUR 26.8 million, as a long-dated impaired receivable was fully provided for with a final charge of EUR 1.65 million.

Profit before income tax was down to EUR 4 million from EUR 7.2 million last year, mainly attributable to higher net finance costs of EUR 2.4 million.

Operating profits produced strong free cash flows, financing entirely the segment’s yearly capital expenditure of EUR 10.9 million. This was largely attributable to:

- the initiation of a new investment plan for a “double jointing” project that will position Corinth Pipeworks in the 500 k Tns USA pipe market of 24m length pipes; this will be completed in 2020.

- selected strategic and operational investments in logistics to enhance safety, optimise cost basis and improve quality.

- selected productivity improvements and cost reduction schemes, across all bare and coating / lining production lines.As turnover was reduced, so was working capital, contributing to a decline in net debt from EUR 183 million as of 31.12.18, to EUR 160 million. Finally, long-term debt was partially refinanced with more favourable terms, through the issuance of a EUR 12.6 million bond loan with a major Greek bank.Subsequent eventsThere are no subsequent events affecting the Consolidated Financial Information presented in this Press Release.OutlookGiven the strong forecast of new projects and the potential of expanding to new markets, the considerable backlog of orders and the growth potential of the offshore cables sector, the overall outlook for the cables segment remains positive for 2020, despite the volatility noticed in the global economic environment. The Corinth plant is expected to retain the high utilisation capacity throughout 2020 and this will be the main driver for the segment’s profitability. The Thiva plant is also expected to operate at high utilisation levels throughout 2020.

Furthermore, in the cable products unit, there are signs of stability in the low and medium voltage cables markets in our main markets in Western Europe, as demand from the construction and industrial use markets has recovered. Such markets, however, continue to experience competitive challenges and the segment will actively seek to geographically diversify its revenue streams through expansion to new markets, such as the Nordic countries and the Middle East.

Finally, the main focus remains the successful execution of existing projects, the award of new ones in existing and new markets and the optimisation of internal processes in order to take advantage of any arising market opportunity.

In the steel pipes segment, the global economic environment in which Corinth Pipeworks operates remains volatile. The imposition of tariffs and antidumping duties by the USA triggered severe competition pressure from local mills to worldwide pipe makers, such as Corinth Pipeworks. Despite these headwinds, the subsidiary remains focused on maintaining its leading position, through new investments and the penetration of new geographical and product markets. It intensifies its efforts to enhance competitiveness and qualify for tenders offered from major Oil & Gas companies. This effort involves, among other projects, the “Manufacturing Excellence” program, an attempt to process digitisation and schemes to introduce Industry 4.0 into its production lines. The transformation of the subsidiary to a more diversified product profile is an essential part of its innovation agenda throughout 2019 and 2020. Corinth Pipeworks maintains its positive outlook for 2020, with the execution of the G.I.G.B. pipeline (Gas Interconnector Greece-Bulgaria) and other major, offshore and onshore, project awards expected.

Despite the current market volatility, Cenergy Holdings expects to maintain the positive momentum gained in 2019. For 2020, there is cautious optimism that the operating environment will improve further as European markets continue to grow and both demand and prices in our operating markets demonstrate positive trends. Conversely, the pandemic of Covid-19 is expected to disturb supply chains around the world, so the subsidiaries closely monitor the developments in regards to the outbreak and are ready to address any short-term demand fluctuations. International political factors will continue to weigh heavily on performance in 2020 while global population growth and urbanisation continue to ensure positive long-term prospects of our industry. Looking ahead, Cenergy Holdings will benefit from the solid order backlog generated and remains well placed to take advantage of improving market conditions in the energy sector and further its companies’ ambitions of remaining significant world players in energy transfer and data transmission solutions.

Statement of the Auditor

The statutory auditor, PwC Réviseurs d’Entreprises SRL / Bedrijfsrevisoren BV, represented by Marc Daelman, has confirmed that the audit, which is substantially completed, has not to date revealed any material misstatement in the draft consolidated accounts and that the accounting data reported in this press release is consistent in all material respects with the draft consolidated accounts from which it has been derived.

he Annual Financial Report for the period 1 January 2019 – 31 December 2019 shall be published on 8 April 2020 and will be posted on the Company’s website, www.cenergyholdings.com, on the website of the Euronext Brussels europeanequities.nyx.com, as well as on the Athens Stock Exchange website www.helex.gr.

About Cenergy Holdings

Cenergy Holdings is a Belgian holding company listed on both Euronext Brussels and Athens Stock Exchange, investing in leading industrial companies, focusing on the growing global demand of energy transfer, renewables and data transmission. The Cenergy Holdings portfolio consists of Corinth Pipeworks and Hellenic Cables, companies positioned at the forefront of their respective high growth sectors. Corinth Pipeworks is a world leader in steel pipe manufacturing for the oil and gas sector and major producer of steel hollow sections for the construction sector. Hellenic Cables is one of the largest cable producers in Europe, manufacturing power and telecom cables as well as submarine cables for the aforementioned sectors. For more information about our Company, please visit our website at www.cenergyholdings.com.

Contacts

For further information, please contact:

Sofia Zairi

Head of Investor Relations

Tel: +30 210 6787111, 6787773 Email: ir@cenergyholdings.com

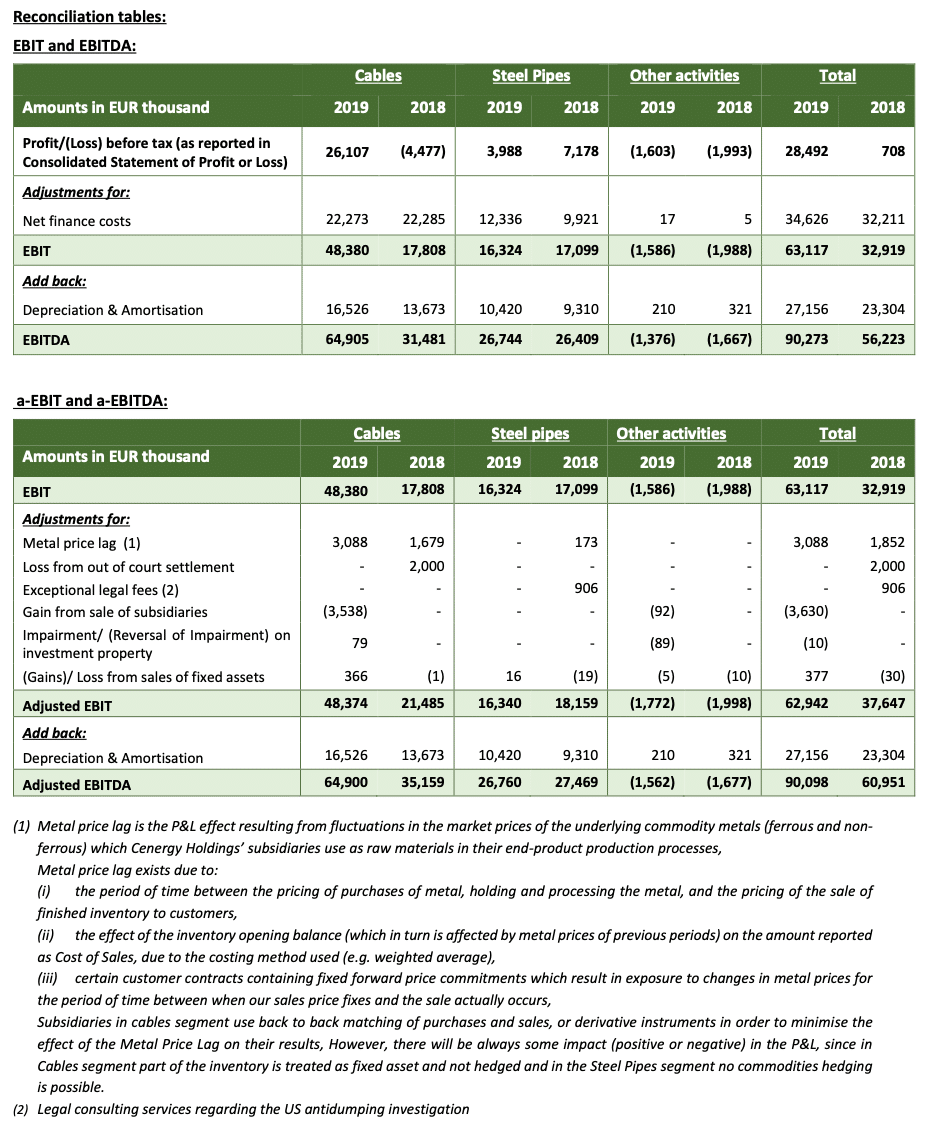

Appendix C – Alternative performance measures

In addition to the results reported in accordance with International Financial Reporting Standards (“IFRS”) as adopted by the European Union, this press release includes information regarding certain alternative performance measures which are not prepared in accordance with IFRS (“Alternative Performance Measures” or “APMs”). The APMs used in this press release are: Earnings Before Interest and Tax (EBIT), Adjusted EBIT, Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA), Adjusted EBITDA and Net debt, Reconciliations to the most directly comparable IFRS financial measures are presented below.

We believe these APMs are important supplemental measures of our operating and financial performance and are frequently used by financial analysts, investors and other interested parties in the evaluation of companies in the steel pipes and cables production, distribution and trade industries. By providing these measures, along with the reconciliations included in this appendix, we believe that investors will have better understanding of our business, our results of operations and our financial position. However, these APMs shall not be considered as an alternative to the IFRS measures.

These APMs are also key performance metrics on which Cenergy Holdings prepares, monitors and assesses its annual budgets and long-range (5 year) plans. However, it must be noted that adjusted items should not be considered as non- operating or non-recurring,

EBIT, Adjusted EBIT, EBITDA and Adjusted EBITDA have limitations as analytical tools, and investors should not consider it in isolation, or as a substitute for analysis of the operating results as reported under IFRS and may not be comparable to similarly titled measures of other companies,

APM definitions have been modified compared to those applied as at 31 December 2018. The modifications are minor and have been made in order to reflect business performance more accurately. The impact of such modifications was rather limited and is presented below.

The change in definition concern the adjustment related to “Unrealised gains/losses on derivatives and on foreign exchange differences”, which has been removed from the calculation of a-EBIT and a-EBITDA, since it was concluded that such amounts are connected with the business performance of Cenergy Holdings companies. Comparatives have been restated accordingly.

The current definitions of APMs are as follows:

EBIT is defined as result of the period (earnings after tax) before:

- income taxes,

- net finance costsEBITDA is defined as result of the period (earnings after tax) before:

- income taxes,

- net finance costs

- depreciation and amortisationa-EBIT and a-EBITDA are defined as EBIT and EBITDA, respectively, adjusted to exclude:

- metal price lag,

- impairment / reversal of impairment of fixed, intangible assets and investment property

- impairment / reversal of impairment of investments

- gains/losses from sales of fixed assets, intangible assets, investment property and investments,

- exceptional litigation fees and fines and,

- other exceptional or unusual itemsNet Debt is defined as the total of:

- Long term loans & borrowings and lease liabilities,

- Short term loans & borrowings and lease liabilities,Less:

• Cash and cash equivalents

Detailed reconciliation between APMs as previously published for 2018 and comparatives of this press release, is presented below.

Reconciliation tables: EBIT and EBITDA: